Fraud in lending is not a new phenomenon. For decades, fraudsters have sought to exploit gaps in financial systems, using false documentation, identity theft, and misrepresentation to secure loans they should not have qualified for. Nowhere is the risk more pronounced than in home lending, where large loan values and complex documentation create fertile ground for fraudulent activity.

With the rise of artificial intelligence (AI), the fraud landscape is evolving rapidly. On one hand, AI has become a powerful enabler for fraud, with new techniques like deepfakes and synthetic identities making it easier than ever for bad actors to deceive lenders. On the other, AI – particularly modern advances in machine learning (ML) and large language models (LLMs) – offers banks, credit unions, and mortgage lenders a set of advanced tools to detect, prevent, and even preempt fraud before it causes harm.

This blog explores the sources of fraud in lending, how AI can increase the risks, and how it can also serve as a critical line of defense.

The Many Sources of Fraud in Home Lending

Fraud in lending comes in many forms, often exploiting the layers of complexity in the mortgage process. Some of the most common sources include:

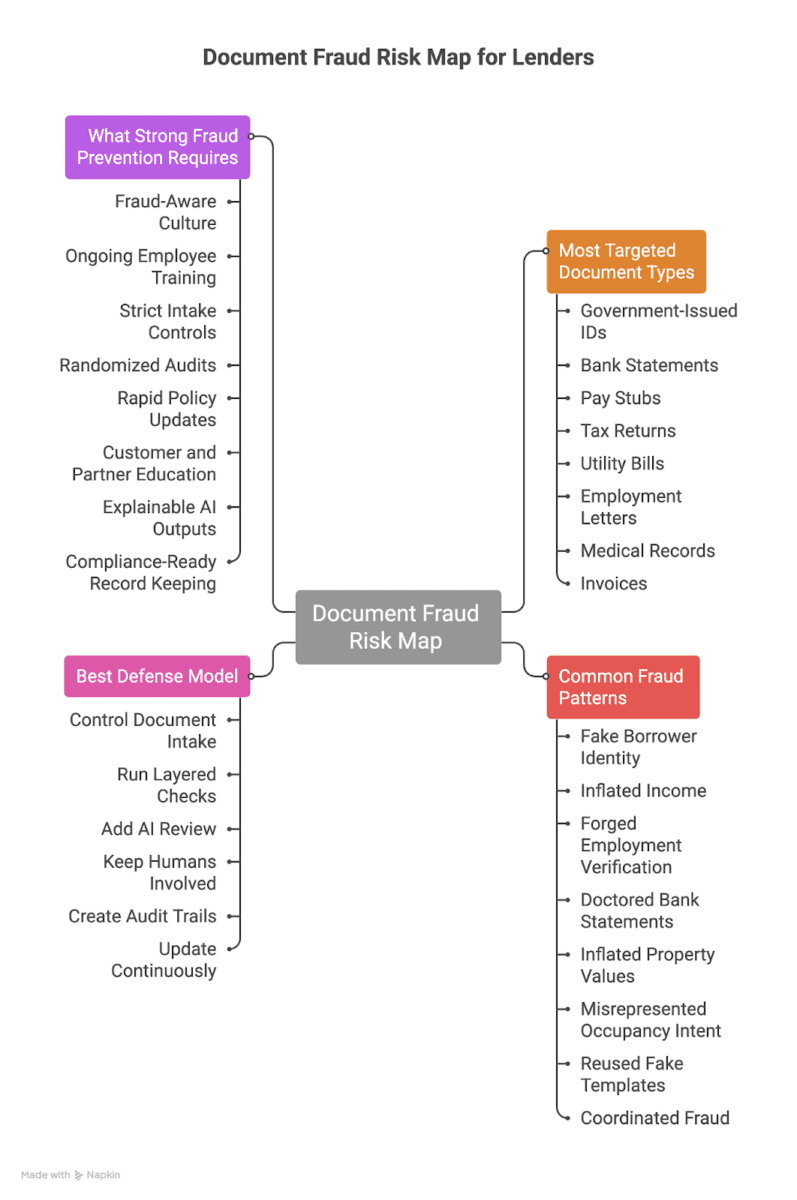

- Identity Fraud – Fraudsters may steal or fabricate identities to secure loans. Traditional methods include falsified driver’s licenses or Social Security numbers. Increasingly, synthetic identities – constructed from fragments of real and fake data – are used to pass as legitimate applicants.

- Income and Employment Misrepresentation – Borrowers may inflate income, falsify pay stubs, or provide forged employment verification to qualify for larger loans than they could otherwise afford.

- Property Fraud – Overstating property values, concealing liens, or misrepresenting occupancy intent (e.g., claiming a home will be a primary residence when it is not) are classic forms of mortgage fraud.

- Document Forgery – Mortgage applications require extensive paperwork: bank statements, tax returns, deeds, and more. Each of these is a potential target for forgery or digital manipulation.

- Collusion and Insider Fraud – Fraud can also come from within. Mortgage brokers, appraisers, or even employees at financial institutions may collude with applicants to manipulate records or misrepresent data.

Industry Applications and Use Cases: Where Document Fraud Hits Hardest

While home lending is a prime target for document fraud, the threat extends far beyond mortgages. Fraudulent documents are used to exploit vulnerabilities across a range of adjacent industries, each with its own high-risk scenarios and consequences:

Banking and Financial Services

Banks and credit unions rely heavily on documents for identity verification, loan approvals, and compliance checks. Fraudsters frequently submit forged IDs, altered bank statements, or fabricated pay stubs to bypass onboarding and secure loans or lines of credit they would not otherwise qualify for. The financial impact is significant, not only in direct losses, but also in regulatory penalties and reputational harm.

Lending and Mortgages

Lenders face unique risks during loan origination and refinancing. Common schemes include submitting fake tax returns, inflated property appraisals, or doctored employment verification letters. These tactics are designed to make applicants appear more creditworthy, exposing lenders to defaults and compliance breaches.

Real Estate and Rentals

Property managers and real estate agents depend on documents like proof of income, utility bills, and identification to vet tenants and buyers. Fraudulent documents can result in unqualified tenants gaining access to properties, leading to payment defaults, property damage, or costly evictions.

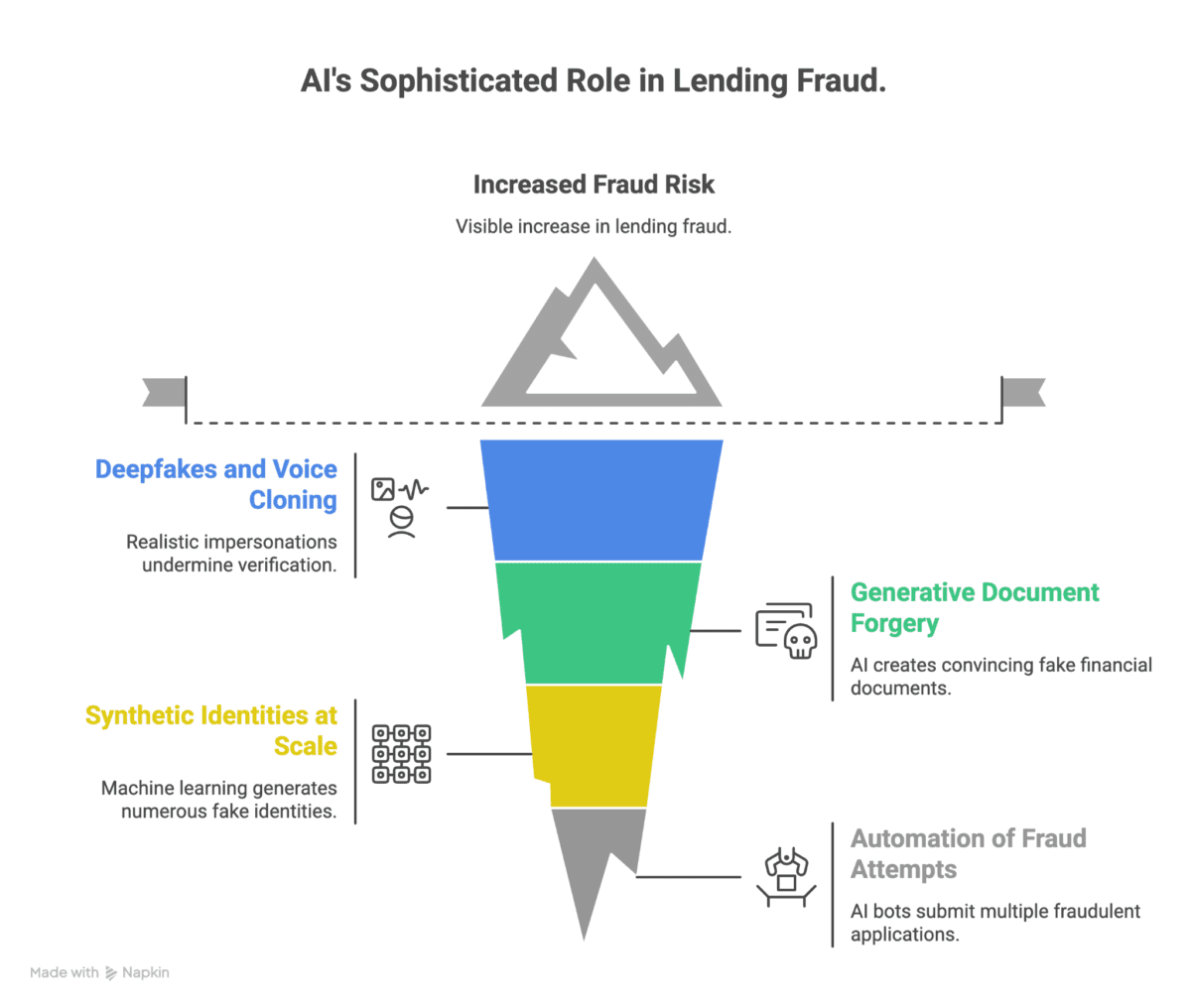

AI as a Tool for Fraudsters

While fraud has long plagued lending, AI is making it more sophisticated and harder to detect. Some of the key enablers include:

- Deepfakes and Voice Cloning – Fraudsters can now generate highly convincing fake IDs, doctored video calls, or synthetic voices to impersonate borrowers, employers, or even notaries. This undermines traditional verification methods that rely on human judgment.

- Generative Document Forgery – AI-powered tools can create realistic pay stubs, tax documents, or bank statements with minimal effort. Unlike older forgeries, these fakes are harder for both humans and legacy fraud detection systems to identify.

- Synthetic Identities at Scale – Machine learning allows fraudsters to generate thousands of plausible synthetic identities that pass basic credit checks, creating large-scale risks for lenders.

- Automation of Fraud Attempts – AI-driven bots can submit multiple fraudulent applications across institutions, probing weaknesses until one slips through.

These developments make fraud more accessible, scalable, and convincing. Left unchecked, they could significantly increase risk exposure across the home lending industry.

AI as a Shield Against Fraud

Fortunately, AI also equips lenders with powerful new defenses. By leveraging advanced analytics, machine learning, and LLMs, financial institutions can significantly strengthen fraud detection:

- Anomaly Detection in Data: AI excels at finding patterns in large datasets. By analyzing years of lending and repayment history, models can identify subtle anomalies in applications – such as mismatches in income-to-expense ratios, irregular property valuations, or inconsistencies in reported employment – that signal possible fraud.

- Document Verification and Forensics: AI models can analyze documents for signs of tampering. For example, image-recognition algorithms can spot inconsistencies in fonts, pixel patterns, or metadata. LLMs can read and cross-check textual data across multiple documents, verifying that reported income aligns with tax records and bank statements.

- Large Language Models (LLMs) in Document Fraud Detection: Modern large language models (LLMs) take document analysis a step further by understanding the context and semantics of written content. Unlike traditional AI models that focus on structure or metadata, LLMs can interpret narrative sections, spot inconsistencies in explanations or letters, and flag unusual language patterns that may indicate deception. For example, an LLM can compare the stated purpose in a letter of explanation to details in supporting documents, or detect when employment history narratives do not align with pay stub data. This semantic layer of analysis helps catch subtle fraud that might otherwise go unnoticed.

- Multi-Modal AI and Layered Detection Approaches: The most effective AI-powered fraud detection systems use a multi-modal approach, combining several advanced techniques. These include computer vision for pixel-level analysis, metadata examination for digital fingerprints, and natural language processing for semantic checks. By layering these methods, AI can cross-validate anomalies—such as mismatched data, unusual formatting, or suspicious language—across different dimensions of a document. This synergy not only increases detection accuracy but also reduces false positives, as inconsistencies must be confirmed by more than one analytical method.

- Biometric and Voice Authentication: Instead of relying solely on passwords or IDs, AI-driven biometrics (facial recognition, voice authentication) can help verify borrower identity in ways that are harder to forge – even in the age of deepfakes. Paired with liveness detection, these tools can expose attempts to use synthetic media.

- Network and Relationship Analysis: AI can analyze relationships between applicants, brokers, and properties to spot suspicious connections. For instance, if multiple loan applications are tied to the same employer or address, it may indicate a fraud ring. AI can also connect the dots across multiple documents and applications, uncovering fraud rings or serial attempts that would be difficult to spot manually. By analyzing relationships between applicants, shared addresses, employers, or document templates, AI systems can identify patterns of coordinated fraud. Graph analytics and relational models help surface these hidden links, allowing lenders to disrupt organized fraud before it causes widespread harm.

- Real-Time, Adaptive Learning: LLMs and machine learning systems can incorporate human feedback “on the fly.” If a loan officer flags a suspicious case, AI models can immediately learn from that signal, improving accuracy for future applications. This dynamic learning contrasts with older, static rule-based systems. Beyond static detection, modern AI systems can continuously learn from new fraud patterns. When a document is flagged by a human reviewer or identified as fraudulent, that feedback is used to update detection models in near real-time. Some systems even employ federated learning, where models improve collectively across institutions without sharing sensitive data. This rapid adaptation is critical for keeping pace with evolving fraud tactics, ensuring that detection methods remain one step ahead of attackers.

- Explainable AI in Fraud Detection: Explainable AI is becoming increasingly important in document fraud detection. Rather than simply flagging a document as suspicious, advanced AI systems provide clear, auditable explanations for their decisions—such as highlighting which fields were inconsistent or which patterns triggered an alert. This transparency not only builds trust with compliance teams and regulators but also helps human analysts quickly understand and act on AI findings.

Compliance, Risk, and Legal Implications in Document Fraud Detection

Fraud detection is not only a matter of operational security—it’s a critical compliance and legal obligation for lenders. Regulatory frameworks such as the US Forgery Act, the False Claims Act, the EU’s FADO system, and the UK’s Forgery and Counterfeiting Act impose strict requirements on document verification and anti-fraud controls. Failure to detect and report fraudulent documents can expose lenders to severe consequences, including regulatory fines, civil lawsuits, and even loss of lending licenses.

Beyond direct fraud losses, weak document controls can inadvertently enable broader financial crimes like money laundering or terrorist financing. Regulations such as Anti-Money Laundering (AML) and Know Your Customer (KYC) require lenders to systematically verify customer identities and document authenticity. Inadequate controls may result in multi-million-dollar penalties and reputational damage.

To meet these obligations, lenders must ensure that their fraud detection systems are not only effective but also explainable and auditable. Regulatory bodies increasingly expect financial institutions to provide clear, documented reasoning for decisions—such as why a document was flagged as suspicious or why a loan application was declined. This requires robust record-keeping for all verification activities, including audit trails of checks performed and decisions made.

Finally, compliance is not a one-size-fits-all process. Lenders must calibrate their fraud detection controls to align with their risk appetite while avoiding both excessive false positives (which may violate fair lending laws) and missed fraud (which can lead to regulatory action). Customizable controls, ongoing policy updates, and regular compliance reviews are essential for maintaining a strong legal defense and consumer trust.

Best Practices for Preventing and Mitigating Document Fraud

While technology plays a critical role in detecting document fraud, a truly resilient prevention strategy requires an organization-wide approach. The most effective defenses combine robust policies, systematic checks, ongoing education, and adaptive processes. Here are key best practices to help prevent document fraud and mitigate its impact:

- Establish a Fraud-Aware Culture

Foster a workplace culture where fraud prevention is everyone’s responsibility—not just the domain of compliance teams. Regularly communicate the importance of vigilance, and encourage staff to report suspicious activity without fear of reprisal. - Ongoing Employee Training

Provide scenario-based training for all employees involved in document handling or verification. Use real-world fraud examples and red-flag checklists to ensure staff can recognize subtle signs of tampering and know how to escalate concerns. - Strict Document Intake Controls

Accept only original, machine-readable digital files (such as PDFs) whenever possible, and require documents to be submitted directly from trusted issuers or secure, verified channels. Avoid accepting screenshots, photographs, or scans unless authenticity can be independently confirmed. - Layered, Systematic Checks

Implement multiple, independent verification steps for high-risk or high-value documents. This may include dual reviews, cross-departmental checks, and the use of standardized checklists to ensure consistency and thoroughness. - Randomized Audits and Continuous Monitoring

Conduct regular, randomized audits of document verification processes to identify vulnerabilities and uncover new fraud tactics. Use findings from these audits to update policies, workflows, and training materials promptly. - Rapid Policy Adaptation

Establish clear protocols for updating document intake and verification policies in response to emerging fraud trends. Ensure that feedback from fraud investigations is quickly incorporated into both technology and human processes. - Customer and Partner Education

Proactively educate customers and third-party partners about the risks of document fraud and best practices for secure document handling. Share tips on how to recognize suspicious requests and encourage reporting of potential fraud attempts.

By integrating these organizational and procedural best practices with advanced detection technologies, lenders can build a multi-layered defense that not only detects fraud but also makes it significantly harder for bad actors to succeed in the first place.

Striking the Balance

The dual role of AI – as both a tool for fraud and a tool against it – highlights the need for vigilance and balance. Lenders cannot assume that traditional fraud controls will be enough in the face of AI-enabled fraud. Nor can they rely on AI alone, as fraudsters are constantly adapting. Instead, financial institutions must adopt a layered strategy that combines:

- AI-powered detection systems

- Logical, rule-based detection to guide and complement AI methods

- Human oversight and expertise

- Continuous adaptation to emerging threats

By treating AI not just as a technology but as an evolving ecosystem – one where offense and defense continually leapfrog each other – lenders can protect both themselves and their borrowers from devastating financial losses.

Looking Ahead

Fraud in home lending is as old as the industry itself, but AI is reshaping the battlefield. Fraudsters are using deepfakes, generative forgeries, and synthetic identities to outsmart traditional controls. At the same time, AI gives lenders unprecedented power to detect anomalies, verify documents, and adapt in real-time to new threats.

The challenge ahead is not whether AI will shape fraud in lending – it already has. The challenge is whether lenders can harness AI quickly and effectively enough to stay one step ahead. Those that succeed will build trust, safeguard assets, and ultimately ensure that the dream of homeownership remains secure.

Join the Conversation!

Subscribe to our biweekly newsletter for a deep dive into where AI technology is going for mortgage lenders, specific use cases, and discuss a “smarter, not harder” approach to innovation.