The pressure to reduce cost per loan and cycle times has never been higher for mortgage executives. The traditional loan manufacturing process, with its heavy reliance on ‘stare-and-compare’ manual reviews, is increasingly seen as a drag on productivity. As TRUE CEO Steve Butler notes, very few understand the entire end-to-end process today – which presents ‘a huge opportunity for change’.

Which is why automated loan underwriting is an opportunity to reshape how lenders manufacture loans, promising a cost-efficient lending process from application to post-close.

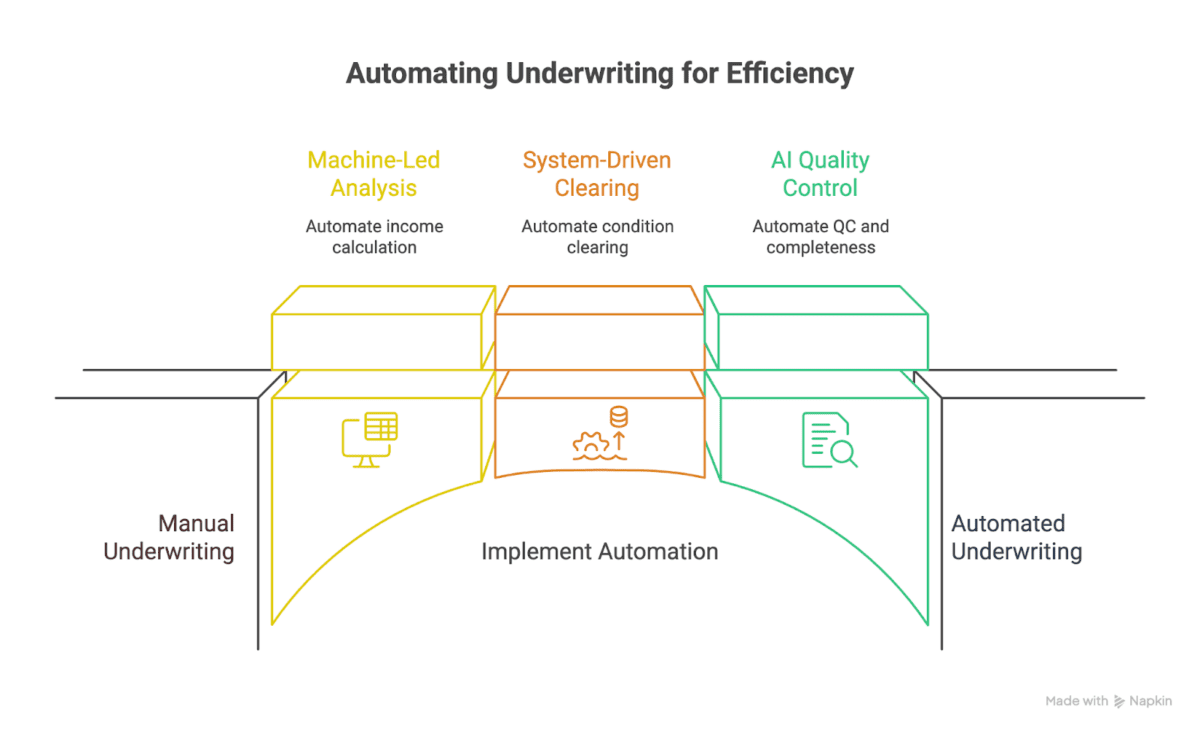

Forward-thinking lenders are embracing automated loan underwriting with one primary objective: to reduce operational costs per loan and to elevate the borrower experience. Explore how automated underwriting, through the TRUE Mortgage Operations Service (MOS) platform, impacts each stage of the loan manufacturing process from setup, income analysis, underwriting decisioning, processing, to post-close.

Why Automated Loan Underwriting Is Overdue

Manual, fragmented processes have long plagued mortgage operations. Loan files pass through numerous hand-offs – from setup to underwriting to post-closing – often involving duplicate data entry, offshore processing teams, and error-prone checklists. This old model drove up cycle times and costs. In Q4 2023, independent mortgage banks lost money per loan on average, due in part to labor-intensive workflows.

By contrast, automated loan underwriting offers a way out of this inefficiency spiral. It leverages AI ‘background workers’ to fully handle specific tasks without human intervention. The goal isn’t partial relief, but end-to-end automation. Because if you still have to manually clean up an AI tool’s output, chances are that you are truly getting a lift in your operational efficiency. Truly automated underwriting means the AI manages each manufacturing step (data intake, analysis, decisioning, etc.) on its own, and that’s where ROI meets the road.

From a strategic viewpoint, automated underwriting directly addresses key C-suite priorities: speed, consistency, and control. It creates a single source of truth in loan data, enabling decisions to happen earlier and more accurately. For example, McKinsey research suggests that streamlining data collection and verification could free underwriters to focus on complex cases, while cutting days of idle time out of the process. The message is clear: lenders who invest in true automation stand to gain a competitive edge in a market where efficiency and borrower experience are paramount.

“If you have to deal with the output of a tool manually, are you really getting a lift? … That’s the problem with assistant-based AI. It still requires human cleanup. But when AI can fully manage a manufacturing step in the mortgage process, the ROI is real.” – Steve Butler, CEO of TRUE

Automated Loan Underwriting in Loan Setup: Fast and Clean Files

Loan setup is the foundation of the underwriting process, but often an operational bottleneck. Manually indexing documents, naming files, entering data into the Loan Origination System (LOS), and performing quality checks can take days for each loan. Many lenders still rely on email for gathering documents and on offshore teams for data entry, which introduces delays and potential errors. Automated loan underwriting in the setup stage attacks these pain points head-on by using AI to ingest and validate documents the moment they are received. Instead of human staff sorting through PDFs and placing them into the LOS, AI document ingestion can classify and index hundreds of pages in seconds.

For example, TRUE’s MOS platform includes an AI-driven document ingestion and classification bundle that prepares a “clean” file for underwriting. Every borrower paystub, W-2, bank statement, and disclosure is automatically identified and filed under the correct category. This not only saves labor but also ensures nothing is missed in the initial file setup. Fragmented point tools (for OCR, indexing, etc.) often require manual oversight or separate integrations. By contrast, a unified MOS approach does it in one seamless step.

Lenders that deploy such technology have cut setup time from days to hours, eliminating overnight offshore prep work and allowing files to flow straight through to automated underwriting systems (AUS) without rework. As True’s CEO Steve Butler emphasizes, it all starts with clean data – “data that’s full, complete, and consistent – across documents and systems” is the prerequisite for instant decisioning later downstream.

An often-overlooked benefit of automating setup is the improvement in data integrity. AI validation cross-checks information across documents (e.g. loan application vs. paystub income) and flags any discrepancies up front. This prevents the dreaded scenario of an underwriter discovering mismatches and kicking the file back to a loan officer for fixes – a common productivity killer in traditional workflows.

By catching inconsistencies early, automated systems produce an auditable dataset that underwriters (and downstream AI decision engines) can trust. Industry experts call the manual verification habit ‘stare-and-compare’. It’s a major drag on productivity that the right AI can eliminate entirely. With high-quality data from the get-go, the loan moves to the next stages of underwriting without the typical stop-start delays.

Automated Loan Underwriting for Income Analysis and Verification

Income analysis is one of the most labor-intensive and critical parts of mortgage underwriting. Lenders must verify and calculate borrowers’ incomes using a pile of documents: paystubs, W-2s, 1099s, tax returns, financial statements for self-employed borrowers, and more. Manually, this is a tedious process prone to error – and any mistakes or conservative estimates can either kill a deal or lead to buyback risk. Automated loan underwriting now excels at income analysis, turning what used to take hours or days into a near-instant highly accurate task.

Consider TRUE’s recently launched Underwriting solution (developed with Candor Technology) that automates manual income work.This AI-driven solution can ingest income documents and deliver a verified, GSE-aligned income decision in just minutes, with little to no human review. In a live pilot, fully automated income analysis enabled loan officers to engage borrowers almost immediately with verified income, rather than waiting days for a back-office calculation.

The productivity impact is enormous: Candor’s existing AI customers saw a 4x increase in underwriter productivity by automating the tedious data review and calculation steps. Crucially, the accuracy and trust level is higher as well. Candor’s engine has produced zero repurchase buybacks on 600,000+ loans to date, thanks to its consistency and rigor. TRUE’s AI has been trained on millions of documents from 4 of the 6 major mortgage insurers, so it can handle the full range of income scenarios (from gig workers to complex self-employed financials) with confidence. When machines handle the income math, underwriters receive clean, audit-ready income data rather than spreadsheets full of manual formulas.

Automating income analysis doesn’t just save underwriter effort – it moves critical decisioning upstream. In the old model, an underwriter might not fully verify income until later in the process, potentially leading to last-minute surprises or borrower disqualifications. With instant income clarity, verified income is available at the point-of-sale to loan officers and upfront underwriters.

This means borrowers can be pre-approved faster and with more certainty, even before they finish shopping for a home. By cutting out back-and-forth verifications, lenders can shave days off the timeline – some claim that approvals happen 70% faster with automated underwriting versus traditional methods. Algorithms apply underwriting guidelines the same way every time, reducing the risk of human oversight or bias. In short, automating income and asset analysis lays the groundwork for faster, cleaner underwriting decisions downstream.

AI-Driven Underwriting Decisioning: From Stare-and-Compare to Instant Approvals

At the heart of automated loan underwriting is the underwriting decision itself – the point where all data comes together to determine if a loan is approved and under what conditions. Traditionally, this step involves an underwriter reviewing the compiled file, running rules (or AUS findings) and checking for any unmet conditions or red flags. It’s laborious and often iterative. AI-powered decisioning aims to collapse this cycle time by instantly analyzing the borrower’s complete profile against lending guidelines and providing a clear decision or list of conditions.

When data is already verified and normalized by earlier AI steps (document intake, income calculation, etc.), the underwriting decision can be made by advanced rule engines without needing a human to sift through documents. Modern AI underwriting platforms (such as Candor’s engine integrated in TRUE MOS) essentially serve as a digital underwriter, applying underwriting guidelines across credit, income, asset, and collateral data in seconds. They don’t just return a simple ‘approve/refer’ like a traditional AUS – they can generate a full approval package with conditions and flags for any issues. This is a huge shift from the days of an underwriter manually comparing each document to guidelines (the “stare and compare” method). As Steve Butler points out, assistant-type AI tools that merely help humans are not enough; the aim is to let AI fully handle discrete decisioning tasks so that the file doesn’t bounce back for human cleanup.

For instance, if bank statements show large deposits, an AI underwriter will flag the need for a sourcing document immediately and even request it from the borrower portal, rather than hoping an underwriter catches it later. Some next-gen solutions have taken this further by automating the running of dual AUS (Fannie Mae’s DU and Freddie Mac’s LPA) simultaneously on each file, ensuring the loan gets the best fit and highlighting any discrepancies between the two automated findings.

The key to AI-driven decisioning is the marriage of trusted data and advanced rules engines. At TRUE, this approach is called ‘background AI workers’ – invisible agents that perform underwriting steps with greater speed and consistency than a human could. The payoff is tangible: lenders adopting such technology have reported automating 70% of manual tasks in the origination process and saving up to $1,500 per loan in costs. Additionally, model-driven underwriting can improve loan quality.

It’s worth noting that this approach doesn’t render human underwriters obsolete – it augments them. With AI handling routine conditions and verifications, underwriters can focus on exceptions and truly complex cases. Early adopters report that their teams can double or triple productivity when freed from rote tasks. In Butler’s words, ‘the LOs now have more time for white-glove service, and the processors can double or triple their productivity’ as background AI takes over the busywork.

This is the ideal: underwriting becomes less about paper-shuffling and more about strategic oversight, with the machine doing the heavy lifting in seconds.

Automated Loan Underwriting Streamlines Loan Processing and Closing

After the initial underwriting decision, loans typically move into processing – clearing conditions, preparing closing documents, and performing final verifications. This stage, too, is rife with manual tasks: gathering updated pay stubs, satisfying appraisal or title conditions, updating insurance info, and assembling the closing package. Automated loan underwriting streamlines processing by orchestrating these post-decision workflows through intelligent automation, ensuring that loans close faster and with fewer errors.

Intelligent Condition Management: One of the biggest time sinks in processing is condition clearing. Processors and junior underwriters can spend hours checking and clearing outstanding conditions. Automated underwriting systems can dramatically reduce this burden.

For example, if the underwriter (or AI) issues conditions, an integrated platform can automatically trigger the fulfillment of those conditions: ordering a verification of employment, retrieving updated bank records via API, or running a compliance check.

Intelligent condition mapping means the system knows which conditions are satisfied by which documents/data and can mark them off in real-time as items arrive. In practical terms, this might look like an AI assistant that continuously monitors the loan file in the LOS for new uploads or data changes, and then updates a central checklist. Lenders have reported that such automation eliminates the mundane task work for loan officers and processors, freeing them to focus on communicating with borrowers and solving truly exceptional issues. By automatically handling routine clears (e.g. verifying a homeowner’s insurance policy or confirming a bank deposit with an API call), the processing stage becomes a smooth, parallel flow rather than a sequence of back-and-forth steps.

Integrating Verifications and Task Tracking: A fully automated loan manufacturing process also tightly integrates third-party verifications and closing tasks. Leading platforms connect with services like credit bureaus, flood certificates, income/employment verification services, and eClosing providers through APIs. The moment a trigger event occurs (say, loan approval or clear-to-close), the system can request any remaining verifications and compile the closing documents package automatically.

Borrowers feel the difference as well – less ‘paperwork anxiety’ and more transparency. Automation can notify borrowers of exactly what’s needed, provide a secure portal to upload any last items, and even generate reminders.

All the while, an internal task dashboard tracks these items to completion, so nothing falls through the cracks. The outcome is a faster clear-to-close, often with far fewer touches. In one case, a lender deploying these tools was able to cut their mortgage processing time in half, with staff reporting significantly lower stress as repetitive tasks were offloaded to AI (per internal case studies).

The Payoff: Effective Lower Costs Per Loan

Adopting automated loan underwriting is not just an IT project, but a rethinking of the mortgage operational model. Adopting truly end-to-end automation in underwriting in an industry that has historically traded off speed for quality (or vice versa) means lenders no longer have to choose – they can have both faster cycle times and better loan quality.