As we move further into 2026, the mortgage market is no longer waiting on transformation, it’s in the middle of it, and lenders are expecting results. From demographic shifts to AI disruption, the next wave of lending will reward speed, intelligence, and experience. What has changed since last year is that the market now has clearer guardrails around how AI must be deployed, governed, and secured in mortgage operations.

Freddie Mac’s March 3, 2026 updates on Use of artificial intelligence and machine learning make that plain. AI in lending now comes with formal expectations for governance, auditability, security, and accountability.

The Volume Surge Is Coming. Will You Be Ready?

Most analysts now project over $3 trillion in originations by 2027 – roughly double today’s volume. That’s 8+ million loan transactions driven by millennial and Gen Z demand, growing female homeownership, and rising immigration. Rate fluctuations aside, the demand is real and inevitable.

For lenders, this raises an urgent question: Can your operations scale with this demand or will they slow you down? If you’re still stitching together siloed tools or relying on manual review to push loans forward, you’re going to fall behind. And as the market scales, the bar is higher than operational speed alone. Freddie Mac now expects mortgage sellers and servicers using AI or machine learning in origination or servicing to maintain documented policies and procedures, assign ownership, secure senior management approval, and review those controls at least annually under its AI/ML guidance.

The Race to Delight the Borrower AND the LO

Two recurring themes dominated the conference:

- Delight the borrower with fast, transparent updates.

- Attract and retain loan officers with a tech stack that helps them earn more.

These goals are deeply connected. Borrowers today expect the “Uber effect,” a real-time visibility into their application and instant confirmation that their documents are received and progressing. At the same time, top LOs want tools that multiply their output, reduce grunt work, and ultimately increase their revenue.

TRUE enables both. By delivering instant, decision-ready data, TRUE allows borrowers to receive actionable updates within minutes of submitting documents. By automating high-effort tasks like document classification and extraction, and instantly surfacing a borrower’s income and asset situation, we give LOs back the time and clarity to close more loans and empower them with decisioning intelligence. When your tech stack drives speed and certainty, it becomes your top recruiting and retention advantage.

Now there is another reason this matters: lenders need systems that also create clean operational visibility into how decisions are supported, how risks are managed, and how controls are enforced. That is becoming part of the borrower trust story and part of the LO enablement story too.

AI Will Drive the Divide

AI is no longer an innovation lab experiment. It’s the engine of scale for the best-performing lenders. Instead of hiring more LOs, AI is helping elite producers scale across new markets, close faster, and handle higher volumes with less overhead.

One speaker at The Gathering noted: “In a few years, the number of licensed LOs won’t double‚ but their loan volume will.” That’s already playing out. Retail market share is shrinking, and smaller lenders are losing ground to IMBs and wholesalers investing in verticalized, AI-driven operations.

TRUE is at the center of this transformation. Our Background AI approach eliminates the need for human review at every stage, while continuously updating file quality and conditions as new documents arrive. No manual review. No system stitching. Just real-time underwriting intelligence. But the divide is no longer only between lenders that use AI and lenders that do not. It is now between lenders that can govern AI in production and lenders that cannot.

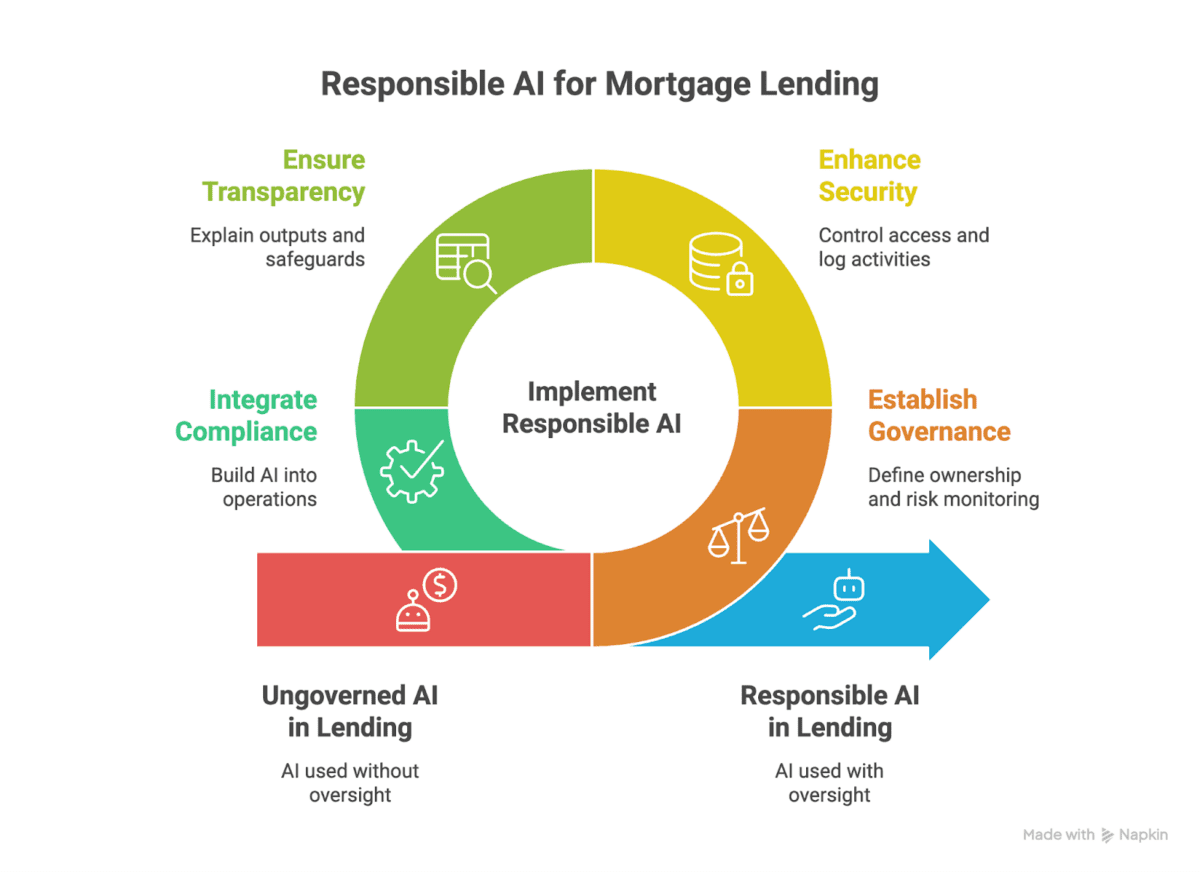

Freddie Mac’s Use of artificial intelligence and machine learning requirements say lenders using AI/ML must be ready to disclose the types of AI used, the purpose and manner of use, and the safeguards in place to mitigate related risks. That changes the standard from “show me the output” to “show me the operating model behind the output.” The requirement also calls for clear governance frameworks for AI adoption, including transparent processes for mapping, measuring, and managing AI risks, documented understanding of legal and regulatory requirements, and accountability structures that define who is responsible for those risks. For lenders, that means AI strategy now has to sit closer to compliance, security, risk, and executive oversight.

Solving for Inclusion, Speed, and Trust

Yes, the focus is on speed – but also on serving more borrower profiles. From aging homeowners exploring reverse mortgage options to gig workers with non-traditional income, lenders need tools that don’t just process data but understand it.

TRUE’s trusted data engine makes this possible. By instantly reconciling docs and extracting the right insights, lenders can serve complex borrowers with confidence and deliver a modern, seamless experience. Freddie Mac explicitly expects lenders to monitor AI systems for performance, security breaches, and bias in its AI/ML section. It also calls out specific AI threats such as data poisoning and adversarial inputs. That means trust in mortgage AI is no longer only about extraction accuracy or faster cycle time, but also about resilience, explainability, governance, and evidence that the system is being monitored over time.

Brokerage Consolidation: Tech Is the New Differentiator

The wave of acquisitions across real estate and lending from Rocket to Lower to Compass signals that the old model of loosely connected systems is fading. Lenders either need to control more of the experience or partner with vendors who provide seamless interoperability.

This is where TRUE stands apart. We don’t require a rip-and-replace strategy. We integrate instantly and operate in the background, acting like invisible coworkers that accelerate cycle times, improve data quality, and reduce overhead. That interoperability story matters even more in a market where lenders are being asked to prove control over cloud environments, access management, logging, vendor risk, and software development practices under Freddie Mac’s Information security requirements. The more fragmented the stack, the harder that proof becomes. The more unified and operationally consistent the system, the easier it is for lenders to manage both scale and compliance.

Information Security Is Now Part of the AI Conversation

Freddie Mac’s updated Information security requirements make one thing clear: AI governance cannot be separated from core security controls. Mortgage sellers and servicers are expected to maintain formal information security programs, annual reviews, data loss prevention controls, vulnerability management, penetration testing, encryption policies, access controls, incident response plans, cloud risk policies, and vendor risk management processes.

The training requirements have also evolved. Freddie Mac says in its Information security section that annual security awareness training should include current cyber threats such as phishing, social engineering and supply chain attacks. AI-powered tactics like deepfakes and targeted phishing, and threats to AI systems such as model inversion, data poisoning, and prompt injection. That is a signal to the market that AI risk is now both an internal operating issue and an external threat vector.

For lenders, this means every AI conversation should now include questions like:

Who owns the model or workflow?

How is access controlled?

What is logged?

How is bias monitored?

What It All Means

Let’s be clear:

- Volume is coming. But the winners will be those who can scale intelligently.

- AI isn’t optional. It’s the new operating system for lending.

- Trusted, instant data is the lever to borrower satisfaction and LO performance.

- Tech stacks are becoming recruiting tools. LOs will flock to lenders that give them speed and certainty.

TRUE delivers all of this now. Not a roadmap. Not a lab experiment. Operational automation that works today.

And now the market has a stronger standard for what “works” really means. It means AI that can be governed. AI that can be monitored. AI that can stand up to audit and security scrutiny. AI that fits inside a lender’s real operating environment, not outside of it.

By year-end, the gap between lenders who act and those who wait will be even wider. At TRUE, we’re helping our clients land firmly on the winning side with AI that doesn’t just support your business but amplifies it. In this next phase of the market, the advantage will not go only to lenders that adopt AI first. It will go to lenders that adopt it responsibly, operationalize it fully, and build it into secure, trusted mortgage workflows from day one.

Join the Conversation!

Subscribe to our newsletter for future blogs about where AI technology is going for mortgage lenders, specific use cases, and discuss a “smarter, not harder” approach to innovation. As the regulatory and GSE environment around AI keeps evolving, lenders need more than trend commentary. They need practical guidance on how to scale automation, strengthen controls, and stay ahead of what the market now expects.