Self-employed borrowers are not ‘hard’ because they are riskier by default. They are hard because the self-employed income analysis workflow forces lenders to do more interpretation, across more documents, with more judgment calls, and with more ways to get it wrong.

Cycle time stretches because the file does not become decision-ready on the first pass. Cost per loan rises because you are paying for repeated reviews, repeated calculations, and repeated condition clearing. Quality risk rises because the same borrower can be calculated differently depending on who touched the file, which worksheet they used, and which assumptions they made.

Fannie Mae streamlines what lenders are expected to do. The lender must prepare a written evaluation of its analysis of a self-employed borrower’s personal income, and the purpose is to determine stable and continuous income available for qualifying. That is the right intent but the issue is that many lenders still execute this intent with manual workflows that do not scale.

Self-employed files are complex. The useful question is where self-employed income analysis can be made faster, more consistent, and more defensible, without creating a new specialist team to run tools. Let’s understand how to get automation to answer that question.

Why self-employed income analysis keeps becoming a bottleneck

Self-employed income analysis is a bottleneck for three reasons that show up in real files, not in vendor decks.

First, the borrower’s “real life income” is rarely the number you can qualify for. Tax strategy, business structure, and one-time events matter. That forces underwriting teams to interpret context, not just read values.

Second, the documentation set is wide. Schedule C, K-1s, 1120S, 1065, business bank statements, P&Ls, balance sheets, 1099s, and sometimes third-party cash flow sources all appear, and they rarely arrive cleanly in one upload. Each new document can change the calculation.

Third, the process is policy-driven and audit-driven. It has to follow the principles in agency guidance, and it has to leave an evidence trail that holds up in QC and delivery reviews.

This is why Fannie Mae points directly to Form 1084 and equivalent tools. The lender may use Cash Flow Analysis (Form 1084), another cash flow analysis method, or an automated tool such as Fannie Mae approved vendor tools, as long as it applies the same principles as Form 1084.

Self-employed income analysis is really a manufacturing step

Most lenders treat self-employed income analysis as an underwriting sub-task. In practice, it behaves like a manufacturing step that determines whether the rest of the file moves downhill or bounces between teams.

If the income analysis is slow, the borrower waits. Income analysis is time-consuming and error-prone, and complex borrower profiles like self-employed and gig workers increase the risk and complexity of qualification.

If the income analysis is inconsistent, the organization pays for rework. Different reviewers can produce different results, which triggers questions from processors, loan officers, and QC teams. That churn shows up in cycle time and cost per loan, even if you do not track it as a distinct metric.

If the income analysis is hard to audit, QC expands. When a lender does not trust its own calculations, the natural reaction is more manual checking. That is how costs rise while teams still feel behind.

TRUE’s CEO Steve Butler draws a line between tools that create outputs and systems that remove work. If you still have to manually clean up outputs, you are not getting operational lift.

Self-employed income analysis has a clear standard, but riddled with inconsistencies

Self-employed income analysis is not a free-for-all. It is guided by established worksheets and principles, and that is why this workflow can be automated responsibly.

Fannie Mae’s Cash Flow Analysis (Form 1084) spells out its purpose in plain language. It is used to prepare a written evaluation of income related to self-employment, and the purpose is to determine stable and continuous income available for qualifying. That statement is the anchor for every self-employed file.

The inconsistencies come from how lenders execute it across large volumes. A manual process depends on the reviewer’s experience, attention, and time. It also depends on whether the right documents were identified and stacked correctly in the first place. If the document classification is off, the income calculation can still look reasonable while being wrong in context.

Self-employed income analysis is harder because borrower profiles are getting complex

Even experienced underwriting teams will tell you that the typical file has changed. Borrowers have mixed income streams. Businesses are structured in more varied ways. Documentation arrives in more formats. It is also arriving later, because consumer apps and mobile uploads shape borrower behavior. Increasingly complex borrower profiles like self-employed and gig workers, plus sensitive qualification criteria, make income analysis more complex and higher risk.

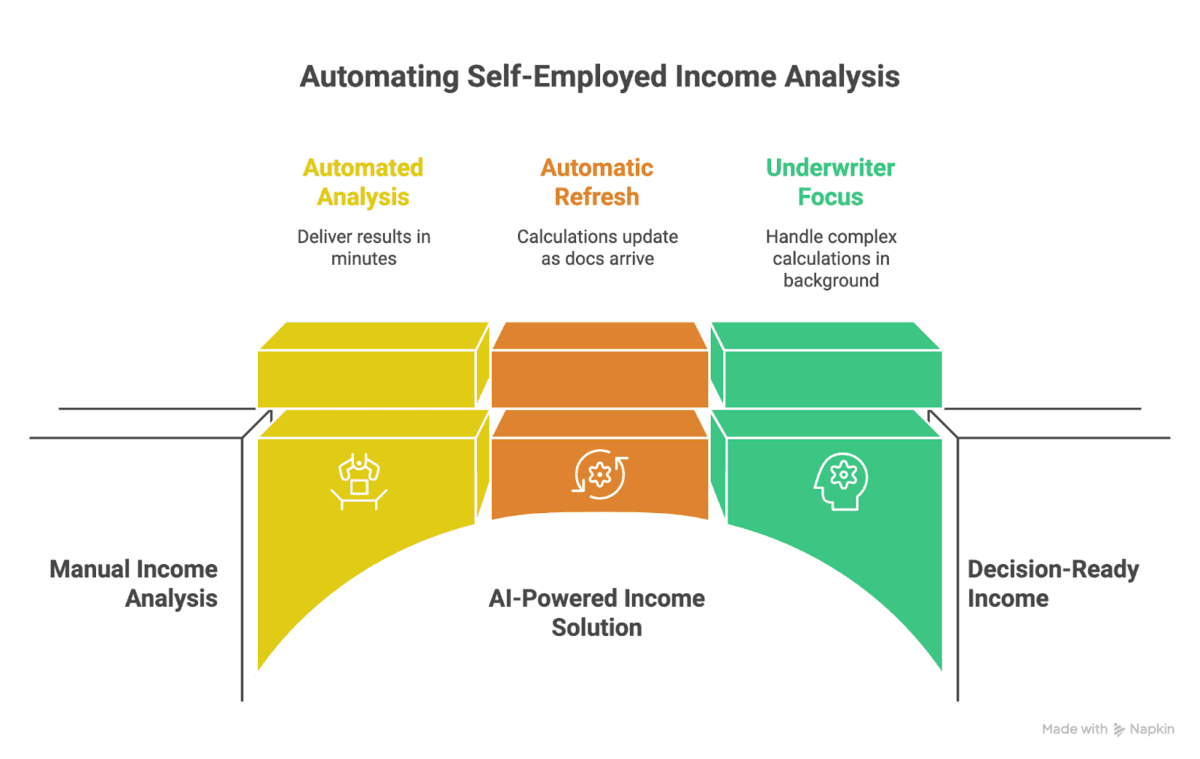

Self-employed income analysis: What done looks like in production

You want a workflow that produces decision-ready income with an evidence trail, without pushing cleanup work onto underwriters and processors. Here are the outcomes you should plan for:

Outcome 1: decision-ready results early

Deliver fully automated income analysis in minutes with little to no human review. That matters because it helps the borrower get certainty, when the lender can lock in the relationship faster, instead of waiting days.

Outcome 2: calculations refresh automatically as docs arrive

Self-employed files change. New statements show up. A revised P&L shows up. A late K-1 appears. If your process requires manual reruns, you create delays and errors.

Your income analysis solution should automatically refresh results as new borrower documents arrive with no manual reruns, and it should support a wide range of income types including self-employed. The system does the repeatable work as new information arrives.

Outcome 3: underwriters focus on judgment, not arithmetic

The real underwriter pain is a blend of these factors: cash flow analyses, transaction reviews, and document comparisons which bog down productivity and extend cycle times, especially with self-employed borrowers or multiple income streams. An AI-powered income solution can handle complex calculations in the background and give decision-ready clarity the moment an underwriter opens the file.

Underwriters should spend time on edge cases and judgment calls, and not spend time retyping numbers into worksheets.

Closing: self-employed income analysis should not be a time-consuming bottleneck

Self-employed income analysis will always require judgment. There will always be edge cases. The problem is that many lenders still run self-employed income analysis as repeatable manual work. They rely on spreadsheets, reruns, and late-stage condition clearing. That makes cycle time unpredictable and cost per loan hard to control.

Fannie Mae gives lenders the framework and even points directly to automated tools that apply the same principles as Form 1084. TRUE believes that the workflow needs to move earlier, run in the background, and refresh automatically as documents arrive.

If you solve self-employed income analysis this way, you do more than speed up underwriting. You reduce the rework loops that eat margin across processing, post-close, and QC, and you give borrower-facing teams earlier certainty that keeps deals from drifting.

Join the Conversation!

Subscribe to our biweekly newsletter for a deep dive into where AI technology is going for mortgage lenders, specific use cases, and discuss a “smarter, not harder” approach to innovation.