Mortgage quality control (QC) is a tough balancing act. You want fewer defects and fewer repurchase surprises, and you still need loans to close and ship on time. The problem is that most QC programs were built for a world where files were smaller, teams were larger, and the last mile was handled by manual checklists and human memory. Today, loan files are bigger, data moves through more systems, and mortgage ops teams are stretched thin. That is why mortgage QC automation is moving from nice-to-have to becoming a core part of how lenders protect margins and keep cycle time predictable.

There is a second problem hiding underneath the first one. QC often becomes the place where you fix what upstream workflows did not catch. When QC turns into a cleanup crew, you pay twice. You pay in rework, and you pay again when upstream teams add more checks “just in case.” That is how cost per loan climbs, while teams still feel behind. Mortgage QC automation is about removing repeatable work, tightening the audit trail, and catching problems earlier. The question for lending executives is where to start and what “good” looks like in their production.

Why Mortgage QC Automation Is Overdue

QC requirements did not appear by accident. The market needs confidence that the loan file supports the underwriting decision and that the documentation is complete and correct. Fannie Mae is clear that lenders must have a QC program that can identify deficiencies in the loan manufacturing process and remediate them, and it ties that directly to delivery eligibility and risk controls.

Still, the day-to-day reality is that QC often runs too late and too manually. Late means the file is already closed, the borrower is gone, and the only options are correction work, delivery delays, or investor friction. Manual means sampling, spreadsheet tracking, and repeated “stare-and-compare” checks across documents and LOS fields. That approach is hard to scale without adding headcount, and it is one reason QC becomes a bottleneck during volume swings.

Mortgage QC Automation Is a Workflow

Mortgage QC automation works when the system can do three things consistently.

First, it can turn messy documents into clean data fields. That includes splitting big PDFs, indexing, naming, and placing docs into the right e-folder. TRUE’s post-close release describes this as splitting single-PDF closing packages into fully indexed, correctly named documents placed into folders, plus signature and date checks, missing document detection, and version control.

Second, it can validate data and link values to source documents. That matters because QC is really about evidence. If your QC team cannot answer “where did this number come from” you end up rechecking everything. The fastest path out is making the evidence trail automatic.

Third, it can drive conditions as part of the workflow, not as a separate afterthought. That is a key difference between ‘QC finds issues’ and ‘QC closes issues’. TRUE calls this workflow ‘intelligently generates and clears post-closing and audit conditions’.

Mortgage QC Automation Starts With File Delivery Reality

You have to deliver loan files in a shape that can be reviewed. Freddie Mac’s electronic file delivery specs show how strict the file requirements can be.

“All post-funding quality control (QC) mortgage file documentation must be delivered to Freddie Mac electronically. Paper is not permitted.”

That one sentence explains why QC automation is turning into a file manufacturing problem. If your internal file shape is inconsistent, you will feel pain every time a loan is selected for review.

Freddie Mac also sets practical limits and rules that lenders must live with, like page and file-size caps and rejected formats, and it recommends stacked PDFs with clear and legible docs. Those constraints shape how lenders build their QC workflows. You either handle this upstream with automation, or you handle it downstream with humans.

Fannie Mae has similar constraints for Loan Quality Connect submissions, including strict naming conventions that drive whether files can be processed correctly. For example, Loan Quality Connect requires loan file names to start with the Fannie Mae loan number and follow defined patterns.

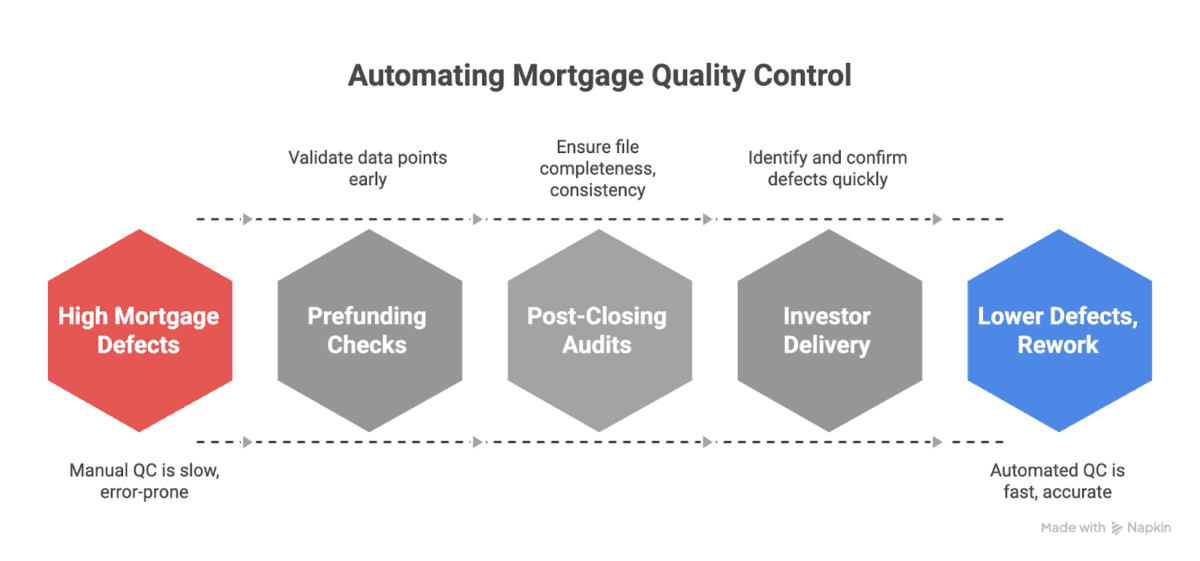

Mortgage QC Automation Has Two Jobs: Lower Defects and Reduce Rework

Mortgage QC automation should reduce defects and rework.

A good way to see this is to break QC into three layers.

Mortgage QC Automation for prefunding checks

Prefunding checks are about preventing bad loans from getting into the pipeline. The more you can catch early, the less you cure later. Mortgage QC automation helps here when it validates core data points against source docs while the file is still in flight. It can flag mismatches between docs and LOS fields, missing signatures, stale versions, and gaps in required documentation.

This is where the background work model matters. A QC system that runs continuously is more useful than a QC system that runs as a once-a-week batch.

Mortgage QC Automation for post-closing audits

Post-closing audits are the last chance to ensure the file is complete, consistent, and defensible before the loan is sold or transferred. TRUE’s post-close release describes this stage as one of the most time-sensitive and labor-intensive processes, and it positions automation as removing manual indexing, removing “stare and compare,” and closing conditions during the audit process.

This is also where portfolio-level QC changes the math. AI review for loans makes it possible to perform 100% QC across portfolios in hours, rather than sampling small percentages. You can disagree with the exact time claims and still take the strategy point: when review cost drops, you can expand coverage and reduce blind spots.

Mortgage QC Automation for investor delivery and cures

Fannie Mae requires lenders to notify Fannie Mae within 30 days once defects identified through QC result in a loan being ineligible as delivered. That requirement drives operational urgency, and it is another reason automation matters. If it takes too long to find and confirm defects, you lose time on fixes and reporting.

Mortgage QC Automation and TRUE MOS: What Gets Automated

TRUE’s MOS framework breaks loan manufacturing into three stages: Loan Setup and Data Quality, Underwriting, and Post-Close. Mortgage QC automation lives across all three, because QC depends on clean files, consistent data, and complete evidence.

TRUE’s post-close enables business outcomes across its lender base: up to 80% reduction in manual document handling, cycle time reductions of up to two days per loan, savings up to $400 per file, and 4x productivity gains in post-close and QC. Whether your lender hits those exact numbers depends on starting point, file mix, and workflow design, the direction is the key takeaway. If QC automation is real, it should show up in labor time and cycle time.

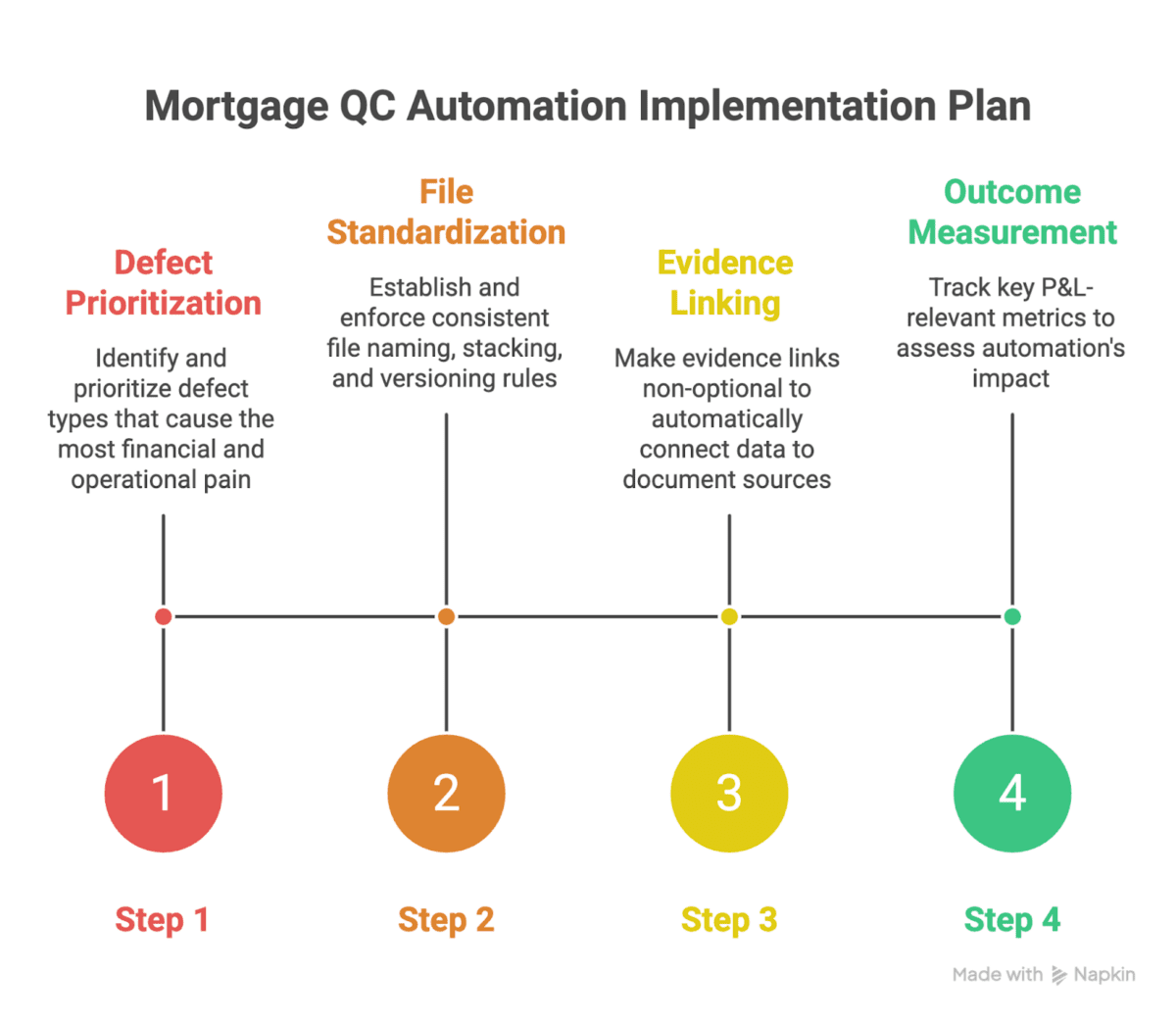

Mortgage QC Automation Implementation: A Practical Plan for Executives

Here is a QC implementation plan that fits how lenders actually run.

Step 1: Pick the defect types that cost you the most

Start with the defects that drive the most rework, delivery delays, and investor noise. Common examples include missing docs, signature issues, mismatches between data and docs, incorrect versions, and conditions that were cleared without the right evidence. Then align automation to those defects first.

Step 2: Force one file shape

You cannot automate QC on a file that has no standard shape. Set one consistent set of rules for naming, stacking, and versioning across your production channels. Use Fannie Mae’s and Freddie Mac’s file constraints as external guardrails that keep your internal standards honest.

Step 3: Make evidence links non-optional

QC is about proof. Ensure the system can link key data points to the exact page and document source. When evidence is automatic, your QC team can focus on exceptions and trends instead of chasing paper.

Step 4: Measure outcomes that matter to the P&L

Executives should measure mortgage QC automation with the same discipline used for underwriting and processing.

Good metrics include:

- defect rate by defect type and severity

- cure time from defect detection to resolution

- touch count per file in post-close and QC

- time from closing to “ship-ready” audited file

- percent of QC work that is exception-only, not full-file rechecking

Closing: Mortgage QC Automation Should Make QC Smaller, Not Bigger

The fastest lenders do not treat QC as a separate department that cleans up defects. They treat QC as a system that keeps the factory honest. Mortgage QC automation fits that model when it standardizes file shape, links data to evidence, and clears conditions with less manual back-and-forth.

TRUE’s MOS approach is built around that idea: pre-built automation across the lifecycle, connected on one data layer, designed to remove rechecking, condition churn, and manual cleanup from application through post-close.

Join the Conversation!

Subscribe to our biweekly newsletter for a deep dive into where AI technology is going for mortgage lenders, specific use cases, and discuss a “smarter, not harder” approach to innovation.