Mortgage leaders keep getting pitched the same promise: “automate the work, close your loans faster, cut cost.”

Then the first loan file hits the system and reality shows up:

- A borrower uploads a statement as photos.

- A paystub has a weird layout.

- A condition gets cleared, then re-opened.

- A vendor sends a “final” doc that is not final.

- A data field is correct in one system and different in another.

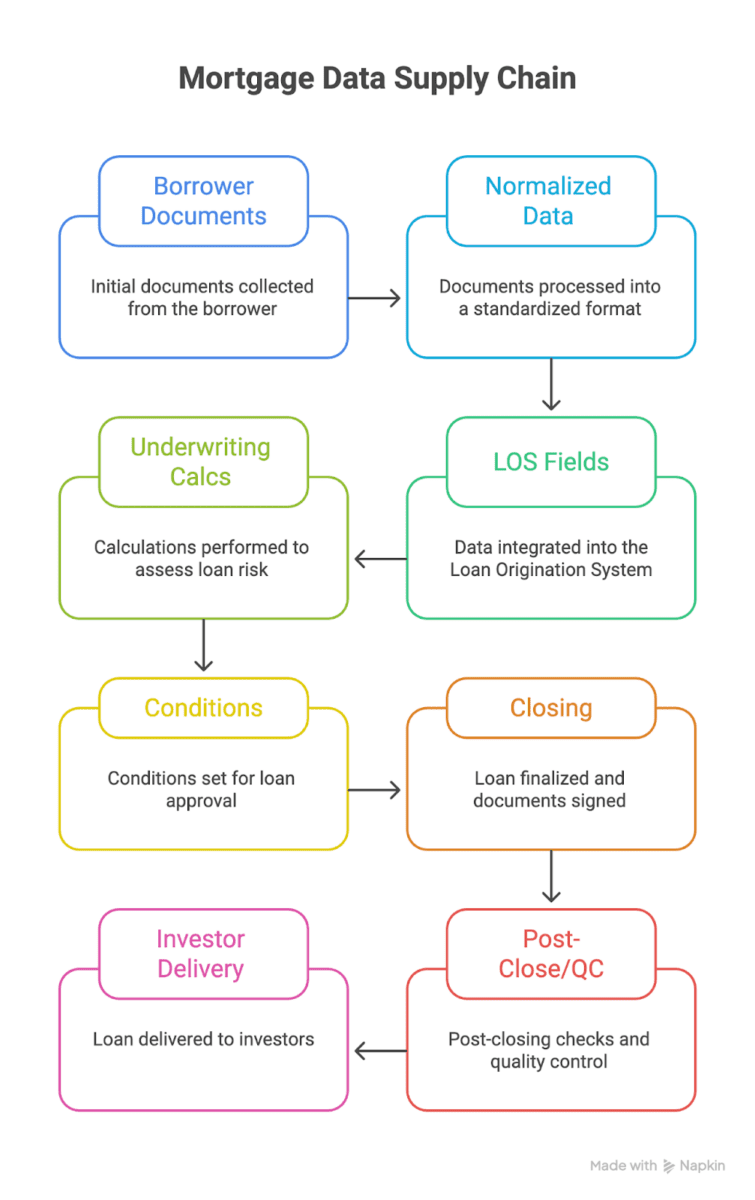

If you do not trust the data, you cannot trust the decisioning, the conditions, or the investor delivery package.

TRUE CEO Steve Butler said it plainly in his HousingWire conversation:

“We’re strong advocates of getting your data right first.”

Here’s how C-level mortgage teams should think about mortgage data solutions, if the goal is faster cycle time, fewer touches, and a higher-quality loan order book.

Why mortgage data solutions have become a standard business practice

Two trends are colliding:

1) Cost pressure is not letting up

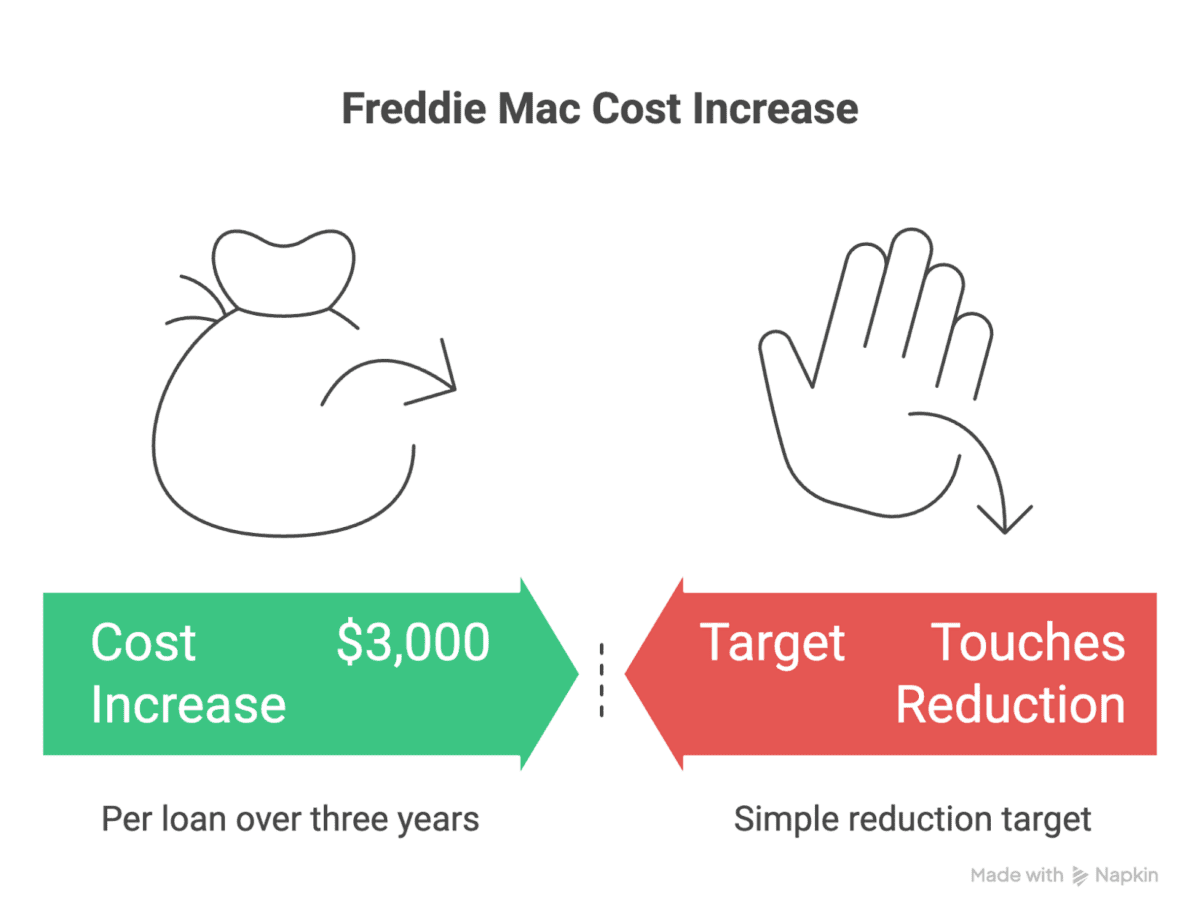

Freddie Mac’s 2024 cost-to-originate study points out that average origination costs have risen by about $3,000 per loan in the past three years, and the gap between top and bottom performers is massive.

When cost per loan rises, boards ask one question:

What are we doing about unit economics?

2) Volume whiplash exposed fragile workflows

When volume drops, lenders cut staff. When volume returns, lenders scramble to hire and retrain. That cycle is brutal for quality and borrower experience. Mortgage data solutions are one of the few levers that can reduce the link between volume and headcount, because the same clean data can be reused downstream.

Mortgage data solutions vs. ‘AI assistants’ that require human intervention

TRUE CEO Stephen Butler’s question on AI implementation becomes the deciding factor:

‘If you have to deal with the output of a tool manually, are you really getting a lift?’

If your team still has to re-key values and reconcile mismatches, then the team continues to engage in stare-and-compare activities, which leads to having a faster way to create exceptions.

TRUE’s angle on building a mortgage data solution is to deploy ‘background AI workers’ – meaning work that gets handled end-to-end as a manufacturing step, not an assistant that produces a draft your team must fix.

Mortgage data solutions start with standard language, then enforce it

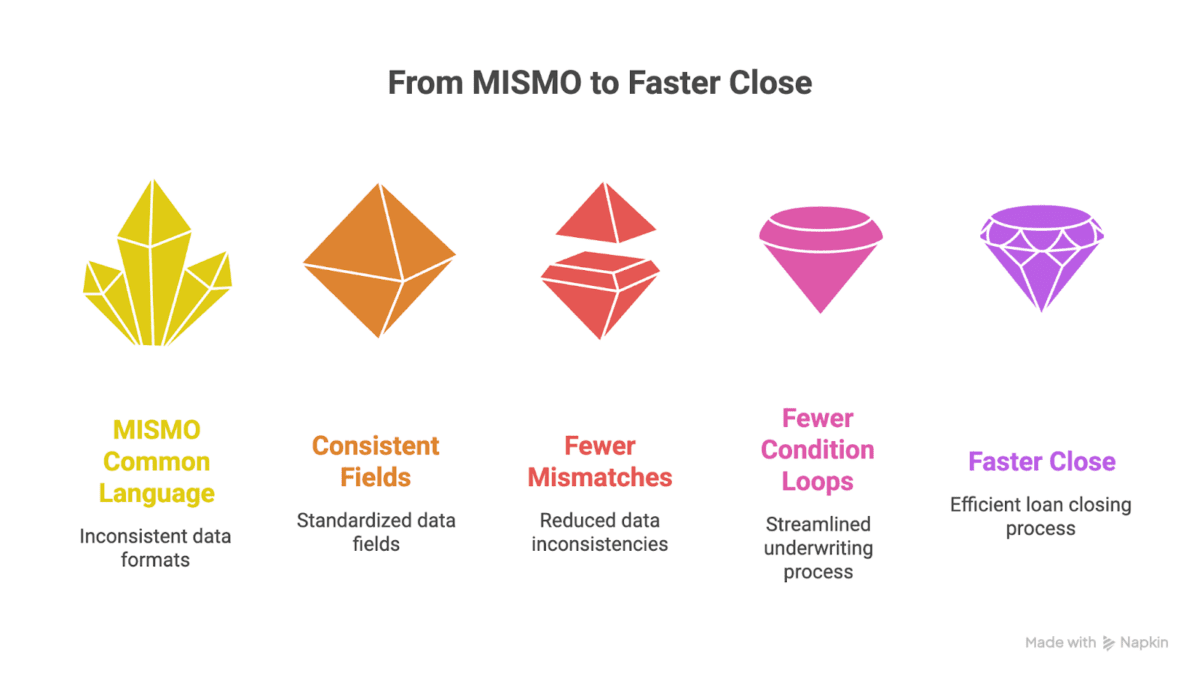

Every lender talks about data standards, then lives with ‘close enough’ when it comes to implementing data quality in their daily operations. Industry standards like MISMO exist, because the industry has learned this lesson the hard way.

MISMO gives the industry a shared data language

MISMO describes its standards as a common language for exchanging mortgage data across the industry. But MISMO standards can provide the definition. Your mortgage data solution needs to ensure that the intake-to-close process enforces and matches these standards every time.

Investor and AUS workflows reward clean data

Fannie Mae’s Day 1 Certainty is positioned around faster closing and better borrower experience. To achieve this, a mortgage data solution should enable the following:

- Automate the system to handle repeatable data validation work early

- Free up your underwriters to spend more time on risk and edge cases

When you push clean data upstream, decisioning and downstream manufacturing become simpler.

What ‘good’ looks like in mortgage data solutions

If you are a COO, CIO, Head of Ops, or Head of Underwriting, you need a set of metrics you could use to evaluate the solutions in front of you.

Data quality outcomes

- Completeness: missing fields drop across core income, assets, liabilities, employment, and property.

- Consistency: the same field matches across docs, LOS, AUS, PPE, and closing.

- Traceability: you can show the source doc and the mapped value without human storytelling.

Workflow outcomes

- Exceptions are flagged early, before underwriting starts

- Human touches per file drop in processing and underwriting

- Conditions become more predictable because the file is ‘cleaner’ earlier

Business outcomes

- Cycle time decreases without raising risk

- Fallout declines because files move with fewer stalls

- Post-close and audit findings decrease

At TRUE, trusted data is treated as a full life cycle problem, not just point extraction. The TRUE MOS platform is built around clean, trustworthy, reusable loan data and ‘manufacturing-level’ automation, so that C-level decision makers are able to go after the true objective behind automating their operations: lower the overall cost per loan.