Post-close is where the work shifts from helping the borrower close to preparing a complete, reviewable file for investor delivery and audit. Documents, signatures, dates, conditions, and versions all have to line up, and the file has to be formally shipped to investors, servicers, mortgage insurers, and the agencies. When post-close slows down, it is rarely because people are under-resourced. It is because the file is messy, the evidence trail is hard to follow, and the organization is forced into late-stage cleanup.

That is why post-close audit automation matters. It reduces the manual work in the last mile while improving consistency in what gets shipped. The goal here is not a new dashboard for post-close managers. The goal is a workflow that takes a large closing package, standardizes it, validates it, and produces an audited file that meets delivery expectations without an ops team doing repetitive sorting and checking.

Why post-close audit automation is overdue

Most lenders already have policies for post-close review and quality control. The issue is the execution model. Post-close is still treated like a back-office queue where teams manually split big PDFs, name and stack documents, run checklist steps, verify signatures and dates, chase missing items, and then do it again when an investor asks for a specific document set.

Fannie Mae is direct about the role of QC and post-closing review in the lender’s control environment. It states that an effective QC program is a key component of the lender’s overall control environment and requires lenders to implement a QC program that identifies deficiencies in the loan manufacturing process and remediates them. That requirement is on point, but it can still create a problem where the remediation becomes manual.

Freddie Mac adds a practical pressure point that many executive teams underestimate until they are right in the middle: QC loan file documentation must be delivered electronically and paper is not allowed. Once you are operating in an electronic delivery world with file size limits, page limits, and format rules, the manual file cleanup model becomes fragile, leading to higher cycle times and defect rates.

Post-close audit automation is a loan manufacturing step, not just for reporting

Post-close teams get measured on cycle time, yet cycle time is usually determined by file readiness. If the file arrives as a single stacked PDF from a settlement agent, your post-close team has to turn that into a clean file structure that can be audited, shipped, and retrieved later. That work is repetitive, time-consuming, and easy to get inconsistent when you are relying on humans to do it across thousands of files.

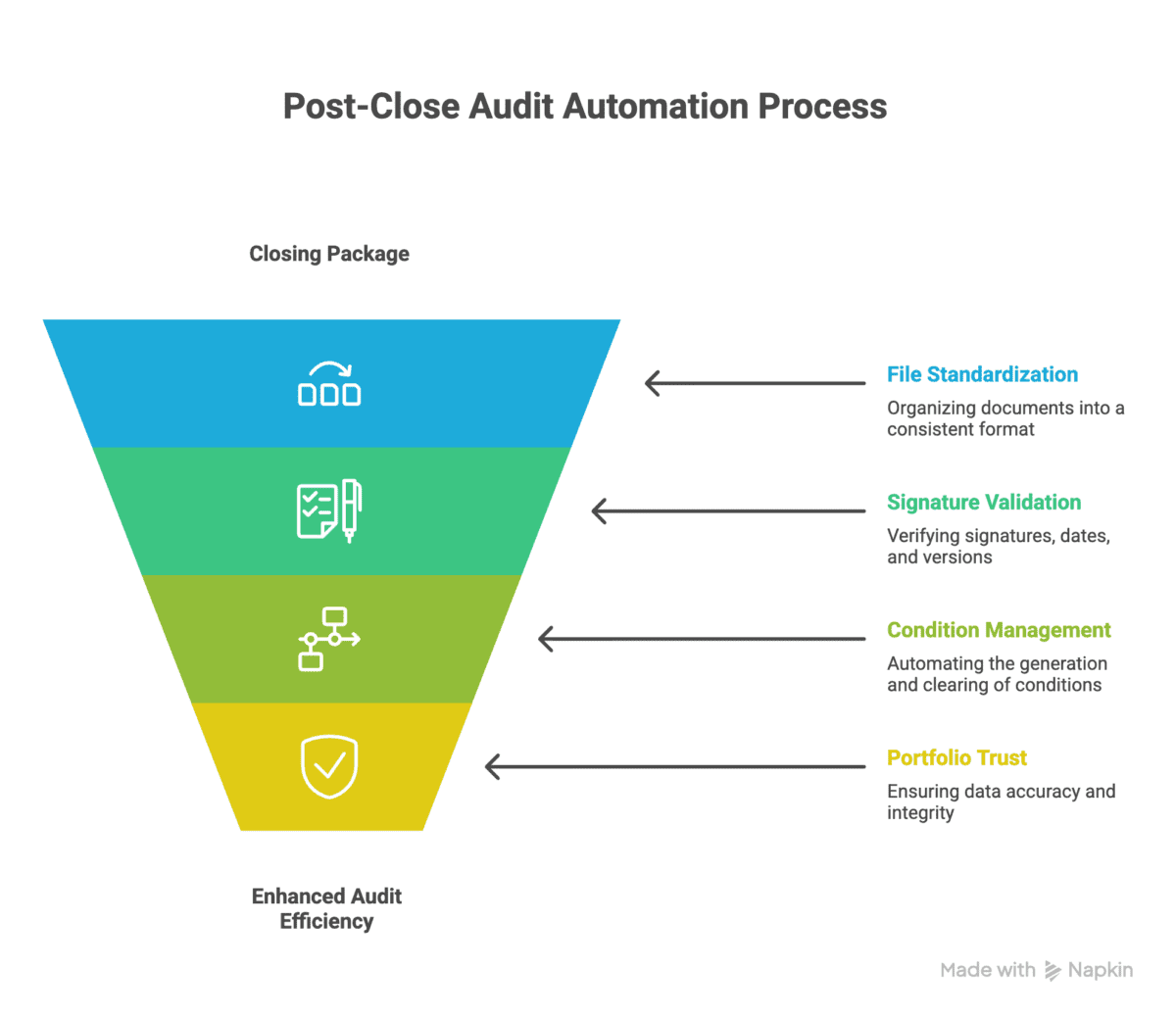

A comprehensive post-close automation system should be able to split large single-PDF closing packages into fully indexed, correctly named documents placed into folders, validates signatures and dates, and generates and clears post-closing and audit conditions.

Post-close audit automation done in this approach ensures end-to-end completion of the loan manufacturing step. It does not describe a tool that helps a person work faster. It describes work that gets done and then written into the file structure your downstream workflows need.

Post-close audit automation must satisfy agency and investor expectations

The last mile is often shaped by how investors and the agencies request and review files. That is why post-close operations should be designed with external delivery constraints in mind.

Freddie Mac’s electronic file delivery specs for QC reviews show exactly where lenders lose time. The specs require a single PDF delivery (bookmarked if possible), clear and legible documents, and it includes size constraints like not exceeding 1,000 pages and not exceeding 100 MB, with files returned if they exceed limits. It also lists formats it will not accept, including multiple PDF file deliveries, Word/Text/HTML, and certain spreadsheet formats.

This is why post-close audit automation is a way to ensure file packaging and document organization are consistent enough that file requests do not become fire drills. On the Fannie Mae side, the Selling Guide has been modernizing and clarifying QC expectations. This is another signal that lenders need workflows that are consistent and defensible

“An effective QC program is a key component of the lender’s overall control environment.”

– Fannie Mae Selling Guide, D1-1-01

Post-close audit automation reduces two kinds of cost

Most executives talk about post-close as a cost center. In practice, post-close creates two types of cost.

The first is direct labor cost. These are the hours spent splitting PDFs, indexing, naming, checking signatures, and chasing missing items.

The second is opportunity cost. When post-close slows, loan manufacturing lines stay tied up longer, investors get files later, and the organization often responds by adding more manual checks earlier in the process. That upstream behavior is expensive and hard to unwind.

What does done look like for effective post-close audit automation

When lenders say they want automation, they usually mean reduced headcount. That is the wrong framing. Post-close audit automation works when it reduces manual work and tightens the evidence trail so your controls are stronger with less effort.

File standardization

The first job is to convert a closing package into a consistent file shape. That includes splitting, indexing, naming, and folder placement. This is where many lenders struggle because document naming and placement rules vary by LOS setup, investor requirements, and internal workflow steps.

Signature, date, and version validation

The second job is validation. Missing signatures, incorrect dates, and wrong versions create defects that turn into investor conditions or delivery delays. This matters because many QC teams spend time verifying what should be straightforward. A consistent validation layer reduces the need for repeated stare-and-compare checks.

Condition generation and clearing

The third job is closing loops. A post-close audit often generates conditions. If conditions are managed manually, they become another queue. When done effectively, automation becomes a workflow engine rather than a scanner. It is the difference between creating conditions and closing them without manual intervention.

Building portfolio-level trust

When done right, post-closing mortgage audit ensures accuracy and integrity of the data supporting the loan decision. Even if a lender does not move to 100% full-file review, the direction is important. When review cost drops, coverage increases, and sampling becomes smarter. It also becomes easier to align QC findings with corrective action because you have more consistent data.

Implementing Post-Close Audit Automation: Measurable Outcomes

If you want post-close audit automation to work well, measure how many touches the automation removed.

A practical scoreboard looks like this:

- Time from funding to ship-ready audited file

- Touch count per file in post-close and audit workflows

- Percent of audit conditions cleared automatically

- Defect rates by defect type (missing doc, wrong version, signature, date, data mismatch)

- File request cycle time from investor or agency sampling

- Return rate on file deliveries due to format, size, or packaging issues

Fannie Mae requires lenders to establish target defect rates and measure performance against targets at least quarterly, with reporting to management. Post-close audit automation should make it easier to track defect types and drive corrective action without building a separate reporting team. When a post-close audit automation works well, your mortgage ops team spends less time remediating files and more time improving your prime objective: lowering the total cost per loan.