W2 borrowers should be the easiest loans you manufacture. They show up with paystubs, W-2s, and a straightforward story. Yet in many lending teams, W2 files still create avoidable drag. Underwriters spend time confirming base pay, trending overtime, and validating bonuses. Processors chase updated paystubs, then re-check the same numbers when a new document arrives. QC re-verifies because the evidence trail is hard to follow. The result is slower cycle time on the very loans that should move cleanly.

That is why w2 income calculation automation matters. It is a practical way to cut touches per file without loosening controls. It also shifts income clarity upstream, so borrowers get answers faster and loan teams spend less time doing repeat checks.

Why W2 income calculation automation is overdue

W2 income rules are well-defined. What makes W2 loans slow is the way lenders execute the work across systems and teams. Income is calculated, then recalculated, then questioned again when a new paystub comes in and confirms something different. Most of that time is not spent making judgment calls. It is spent reconciling, re-entering, and re-checking.

Fannie Mae is clear that documentation standards do not change just because a file is underwritten differently. The requirements for paystubs, W-2s, and tax returns still apply, and they must meet the same requirements without regard to the underwriting method. Automation has to execute the same standard, faster and more consistently.

At the same time, policy complexity has increased. Income assessment has to cover stability, adequacy, and likelihood of continuance, which Fannie Mae calls out as key factors in qualifying the borrower. That is why many teams fall back into ‘stare-and-compare’ habits. They are trying to be safe, so they keep adding steps. W2 income calculation automation is the cleanest place to remove steps without raising risk, because the inputs and the expected outputs are already defined.

What W2 income calculation automation means in practice

Many vendors describe automation as faster extraction. W2 income calculation automation should mean the system can do four things end-to-end:

- Recognize and classify the right documents (paystub, W-2, VOE, year-end paystub, employment verification report).

- Extract and normalize the right fields (base pay, hourly rate, YTD, bonus, overtime, tips, commissions, pay period dates).

- Apply policy logic for stability and trending in a consistent way, then produce an income conclusion that is clear and auditable.

- Write back results into the LOS and underwriting workflow so the file keeps moving, instead of creating a new portal and a new queue.

Steve Butler, TRUE CEO, has a simple litmus test for whether automation is real: “If you’re going to require a human to deal with the output of it in mortgage, then are you really getting a lift?” That applies directly to W2 income. If your underwriters are still cleaning up outputs and re-keying values, you have not removed the work.

TRUE positions its approach as ‘background AI workers’ inside the MOS platform, meaning the system completes the step and reduces human cleanup across stages of manufacturing. The core idea is that automation has to behave like manufacturing, not like a helper tool.

The hidden reasons why W2 income still slows loans

W2 income looks simple until you open the file. Here are the recurring reasons W2 files still slow lenders down.

W2 income calculation automation has to handle mixed pay types

Many borrowers have a base income plus bonus, commission, overtime, or tips. Underwriting has to evaluate each income type under its own rules, then determine what is stable and likely to continue. Fannie Mae’s Selling Guide breaks income assessment down into sections, including base income and other employment-related income categories.

If your workflow treats W2 as one number, you end up with rework, because someone will later split base from variable pay and run trending. W2 income automation should separate these income components from the start and keep the evidence clear.

W2 income calculation automation has to solve the ‘documentation mismatch’ problem

Paystubs and W-2s can disagree on dates, job status, or pay amounts. That mismatch forces follow-ups. Fannie Mae also notes that a year-end paystub reflecting earnings from the entire year can be acceptable in lieu of the W-2. That nuance matters when borrowers cannot quickly provide a W-2 and teams need an alternate path.

Automation that can reconcile documents and show why a conclusion was reached reduces the back-and-forth that keeps files in limbo.

W2 income calculation automation has to support trending logic without manual spreadsheets

Income assessment often requires looking at YTD earnings and comparing prior years to confirm stability and trend. Teams often do this with worksheets. Then the worksheet lives in a folder, separate from the LOS fields, and QC rechecks the math anyway.

Automation should keep the math and the evidence linked, so the same result can be reused in underwriting, processing, and post-close review.

How TRUE frames W2 income calculation automation inside MOS

TRUE’s MOS framing divides manufacturing into stages: Loan Setup and Data Quality, Income Analysis, and Processing through Post-Close. W2 income work sits inside Income Analysis, and it depends heavily on clean setup and document readiness upstream.

The MOS platform delivers verified, GSE-aligned income clarity ‘in minutes’ and makes it accessible to loan officers and branch teams, not just underwriters. That shift matters because W2 borrowers shop quickly. If your teams can confirm income while the borrower is still engaged, fallout drops. Traditional income analysis can often takes hours or days due to manual review or offshore outsourcing, which is why TRUE’s MOS platform enables instant, verified income analysis as the key driver.

W2 income calculation automation: What ‘done’ looks like

If you are evaluating automation, the goal is not to extract faster. The goal is to change the operating model.

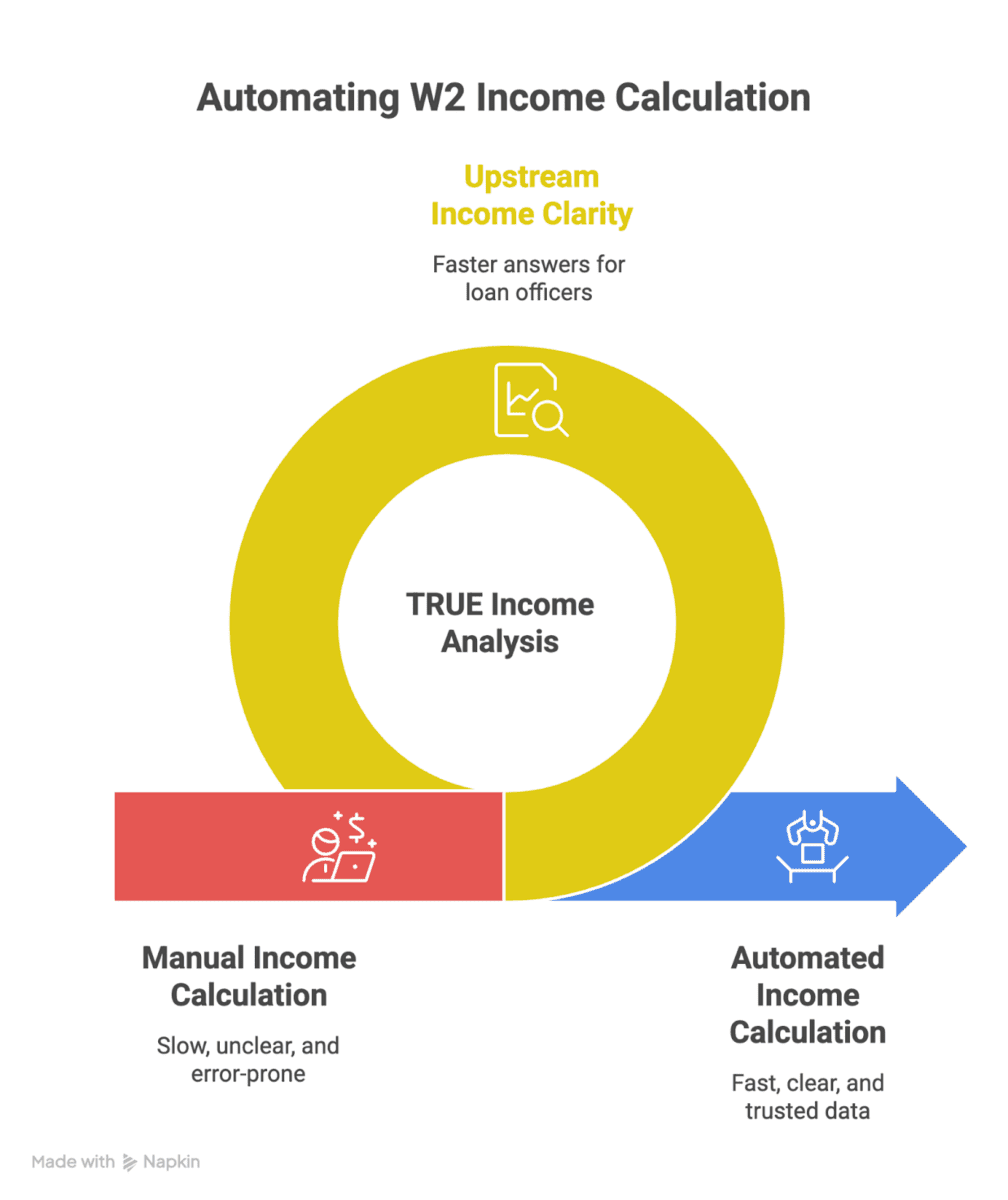

Outcome 1: Income clarity moves upstream

Decision-ready income should be available earlier, including to loan officers, so the borrower gets a faster and clearer answer. This matters for conversion as much as it matters for underwriting efficiency.

Outcome 2: Fewer reruns when new docs arrive

A common W2 pain point is reruns. A new paystub arrives, or a VOE updates, and the file triggers rechecks. TRUE’s income analysis automation emphasizes outcomes that can refresh results as documents arrive, reducing manual reruns and late resets.

Outcome 3: Audit-ready evidence without separate spreadsheets

If your QC team redoes income math, you have a data trust problem. TRUE repeatedly positions “trusted data” and “trusted decisioning” as the way to reduce rework across the workflow. That is what an executive should want: one consistent decision trail.

Closing: W2 is where the factory should run clean

W2 income is a breeze to process compared to self-employed income. It is also where lenders should be proving that their manufacturing line works. If you cannot move W2 loans quickly with clean evidence trails, you will struggle to scale anything more complex.

W2 income calculation automation is a strong starting point because it is repeatable, policy-defined, and highly measurable. When it is done right, it reduces touch count, shrinks condition loops, and makes QC easier because the evidence is already linked. That is the kind of operational lift mortgage executives can defend, in both cost per loan and risk controls.

Join the Conversation!

Subscribe to our biweekly newsletter for a deep dive into where AI technology is going for mortgage lenders, specific use cases, and discuss a “smarter, not harder” approach to innovation.